Just days after the shock announcement that Brett Redman was leaving his role as CEO of AGL, Richard Van Breda, CEO of Stanwell has also resigned.

Richard has been the CEO of Stanwell since 2012 and has led the company through many challenges including potential asset sales, the retirement of Collinsville and Swanbank B power stations, droughts, a drop in the spot and contract prices and COVID-19.

Earlier in the week Richard announced that Stanwell had long term plans to transition from a largely coal fired generator to a renewable energy and storage business.

He said, “We are taking early steps to bring our people, communities, unions and governments together to put plans in place.” Mr Van Breda also said “Over the coming years, Stanwell will respond to the renewable energy needs of our large commercial and industrial customers through the introduction of new low or zero emission generation technologies”.

Mr Van Breda will continue full time in the CEO role until May 28 when an Acting CEO will take over and the process to recruit a permanent replacement will commence.

With the downturn in the Electricity market, most companies are finding it hard to make a profit. As a sign of things to come Origin Energy has downgraded its guidance for full-year profit.

Previously, Origin had highlighted it was partially insulated from the impacts of the Electricity market downturn. However, following a ruling on a gas dispute with Beach Energy, this has resulted in Origins gas supply costs increasing by up to $40M this financial year, then increasing to $80M the following year. The dispute occurred due to Origin and Beach Energy not being able to agree on pricing under the contract which is reviewed every three years.

Origin has previously amended its guidance for gross earnings to $1.14B, with earnings expected to be $1.02B. As a result of this news, shares in Origin dropped 4.5%.

Beach Energy is a major supplier of gas to Origin. The gas pricing determination will affect the cost of gas and impact the profits from Origins network of end users and power generation assets.

Origin’s coal fleet profits have been impacted as wholesale prices fall. Origin was hoping gas would be the solution to it’s drop in profits. Chief Executive Frank Calabria said the company is “disappointed in this decision which we believe is wrong and entirely inconsistent with our prior experience in the gas market”. “This will result in a gas price that does not reflect market prices, and it is therefore a very poor outcome.”

Origin will still benefit from the performance of Australia Pacific LNG which Origin owns 37.5% of and is expected to return cash distribution of $650M.

Origin guidance of “challenging” conditions in energy markets remain unchanged and expect returns not to improve in its electricity and gas businesses until the 2022 financial year

Last week it was AGL. Is it now Origin Energy’s turn to announce a demerger?

On Thursday Origin Energy’s CEO put an end to the speculation, saying that they would not be taking AGLs lead and demerging their business for now. In the announcement, AGL’s rival highlighted the benefit for the company to stay whole, but to diversify their earnings.

Commentary around the potential demerger has been highlighted by Edge and others over the last couple of months. Edge saw an opportunity for Origin to either spin off its retail business or split the business into 2, being electricity and gas.

Origin is a complicated business, operating across both electricity and gas, and across wholesale and retail. Parts of the business are also tied up in joint ventures such as the LNG export terminals in Australia and its part share in Octopus Energy in the UK. Origin has reported that it ‘‘will continue to assess the portfolio’’.

Origin’s structure is different to AGL’s. Origin’s LNG business is currently propping up its domestic gas and electricity business units. If the pressure from a dropping international gas price puts stress on LNG returns, we may well see Origin have a closer look at its portfolio and structure.

Currently the APLNG venture returns $800M to Origin after tax.

CEO Mr Calabria said “Origin’s energy market business already looks very much like the ‘’new AGL’’’, with the notable difference that Origin has a more gas fired portfolio, with Eraring (the only coal unit) flagged to shut down from 2030.

Mr Calabria has also shown limited expectations in the short term for the energy industry, unless we see hotter summers leading to higher demand or the shutdown of coal power generation as a result of the unsustainable low spot prices. He remarked that the market is in an ‘‘unstable equilibrium’’ as an increased amount of renewable generation enters the market and the resulting wholesale prices squeeze profits of the generators and retailers.

As we move through this unstable equilibrium, Origin sees opportunities for State governments to take NSW’s lead and introduce policies to motivate investment rather than wait for increases in spot price.

NB: Spot prices have historically been the leading indicator for investment in new generation. If government led roadmaps became predominant, it may lead to a smoother transition to a renewable future and the orderly retirement of coal and gas generation.

So, with APLNG subsidising Origin’s other business streams we are unlikely to see a demerger, but can Origin utilise this upper hand in the market to push out the competition – demerged or not?

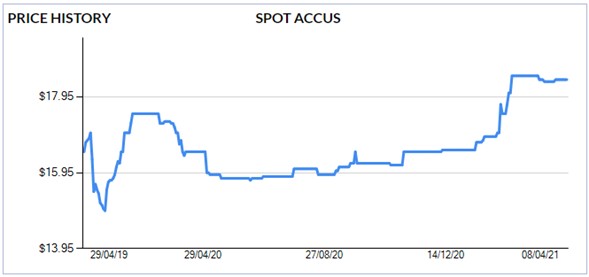

As the next round of auctions are set to take place under the Emissions Reduction Fund, prices for Australian Carbon Credits (ACCU) have increased steadily since January and are now trading at $18.40 per certificate, 10% higher than in January.

The growth in the ACCU market is partially from the Federal government’s Safegaurd mechanism, but also due to an increasing number of companies implementing zero emission targets and using ACCU’s to offset their emissions.

As more companies choose to aim for a net zero emission position, the supply / demand balance in the ACCU market has shifted and the price of the commodity is increasing. Some forecasts predict ACCUs could reach as high as $45 per certificate by 2030.

The biggest jump in the price for ACCUs was recorded in February when the Prime Minister endorsed a net zero target by 2050.

As highlighted in previous articles, many companies are responding to shareholder pressure to reduce emissions and decarbonise. The European market, Emissions Trading System (ETS), a block of 27 countries, has seen EU carbon permits jump from €23 in November to €41 in March. They were trading closer to €5 only two years ago. The price increase has been the result of the EU’s tougher climate change policies.

Large emitting companies had until February 2021 to purchase their ACCUs to comply with their Safeguard liabilities, hence the increases in price. However as seen from the chart above the prices of ACCUs has remained high. This leads to the assumption that voluntary purchases of ACCUs are maintaining upward pricing pressure.

Across Australia, large emitters such as AGL have been joined by large energy users including the Coles Group and Woolworths to commit to net zero greenhouse gas emissions by 2050. Other large gas and petrochemical exporters have started to sell carbon neutral LNG and other carbon neutral products, this is achieved by carbon offsets such as ACCU’s.

As the demand for carbon offsets increases the ACCU price is likely to continue to rise until cheaper abatement solutions develop such as improved farming practices resulting in improved soil carbon storage and broad acre management such as Savanna burning.

Common to all markets, the offset market is currently in a state of flux. Demand will most likely increase the price of ACCUs while new project and pressure from international carbon offsets will put downward pressure on prices. The positive takeaway is businesses are clearly proactively moving to reducing their carbon footprint.

Along with Easter, last week brought with it the close of Quarter One (Q1). Prices across the NEM were the lowest we have seen since Q1 2015. Prices were down from the same quarter last year by:

21% in QLD

56% in NSW

68% in VIC and

37% in SA

In comparison to the five-year Q1 average from 2016 to 2020, Q121 prices for the regions were down:

54% in QLD

55% in NSW

73% in VIC and

61% in SA

This compared to operational demand declines of:

3% in QLD

9% in NSW

7% in VIC and

14% in SA

The real story lies in the quantity of utility scale solar and wind entering the regions on any given day. Australia’s energy transition is well underway, with large quantities of utility scale solar and wind generation supplying high percentages of our regional demand in any given day.

On Friday, 26th March we saw approximately 1,700MW of utility scale solar and wind generation supplying Queensland. That’s nearly 30% of the Q121 average during daylight hours.

Whilst there is no shortage of renewable developers and investment funding to shift our transition into yet another gear, there remains some major obstacles, and the reality is prices like that seen in Q121 are part of the problem.

On a macro level grid capacity and energy policy, uncertainty remain speed bumps to an even faster shift to renewable energy resources. Closer to the deal tables however, securing revenue certainty at bankable levels is becoming increasingly impossible.

Developers are relying on large Commercial and Industrial (C&I) consumers to pay the price to meet sustainability objectives. The pool of potential C&I off-takers is drying up fast.

Q121 brought with it the early retirement announcement by Energy Australia (EA) for Yallourn Power Station. With prices like that seen in Q121, this is just the start. Many generators will be coming off higher forward contract prices and shifting into periods of much lower forward contract prices and / or low spot prices.

Revenue at these levels is not sustainable. However, there is no denying that traditional energy generators will need to delay the inevitable for as long as possible. Whilst the renewable projects remain in hiatus, relying mostly on sustainability driven C&I off-takers, the market will struggle to shift to the next gear in our energy transition.

As soon as coal (in particular) starts to break, and plants start to mothball and / or retire earlier than otherwise expected, increasing spot prices will yet again become the oxygen that breathes life back into the utility scale development pipeline.

And so, the cycle will continue until batteries (including pumped storage hydro) finalise our move to a renewable energy future.

At an Asian Investment Conference last week, Iron ore miner Andrew Forrest detailed his company’s plans to produce the world’s lowest cost green hydrogen and green ammonia via a potential pipeline of 1000 GW of renewable energy assets.

The Fortescue Group announced the companies within the group would aim to achieve carbon neutrality on its Scope 1 and 2 emissions by 2030, through absolute emissions reduction rather than the use of offsets.

The Fortescue boss plans on developing green iron ore, running his trains and trucks on renewable energy and operating ships on green ammonia. He also invests heavily in renewable energy and clean technology through his private company Squadron. Squadron recently took a 75% stake in WindLab, a wind energy development company and is potentially a cornerstone to Forrest’s clean energy ambitions.

As part of his plan to provide Australia with dispatchable renewable energy, Forrest has declared he will meet federal Energy Minister Angus Taylor’s April deadline for a commitment to build new generation capacity in NSW, if state and federal development approvals and underwriting occurs.

Squadron Energy will develop a 635MW gas and hydrogen-fired power station at Port Kembla. Equipment supply will be fast-tracked to meet first generation in 2023 in line with the closure of Liddell power station. This may also prevent the federal government building its own 1,000MW gas turbine using conventional gas.

Initial plans for the power station were larger, however AEMO flagged the 1000MW single unit to be a potential risk to system security. The proposed smaller 635MW unit now meets AEMO guidelines with Squadron expected to build a second generator of the same size at the same site.

The proposed $1.2B Port Kembla power station would be located next to the LNG import terminal under development. Squadron was already investing “millions of dollars” in the power project, which would be complemented by hundreds of megawatts of wind power projects planned by the newly acquired wind developer Windlab.

As wind and solar power is key to the success of Forrest’s clean energy ambitions, he has put pressure on politicians on the west coast as well as the east coast to allow more development of renewable energy. The West Australian government is set to implement changes to land tenure laws so thousands of hectares of land covered by cattle stations can be turned into large scale solar and wind farms to support green hydrogen production.

So, with Australia’s new leader in renewable generation and emission reductions emerging, backed by his proven business ability, the renewable energy industry, and the energy sector as a whole, looks like we are in for a shake-up.

Earlier in the week Richard announced that Stanwell had long term plans to transition from a largely coal fired generator to a renewable energy and storage business.

Earlier in the week Richard announced that Stanwell had long term plans to transition from a largely coal fired generator to a renewable energy and storage business.

Along with Easter, last week brought with it the close of Quarter One (Q1). Prices across the NEM were the lowest we have seen since Q1 2015. Prices were down from the same quarter last year by:

Along with Easter, last week brought with it the close of Quarter One (Q1). Prices across the NEM were the lowest we have seen since Q1 2015. Prices were down from the same quarter last year by: