Hydro Tasmania have signed its first deal for the energy stored in its system.

The financial contract between Macquarie Group, Shell and Hydro Tasmania sells the rights to the energy stored in Hydro Tasmania’s network of water storage. Hydro Tasmania sell the right to the energy during the parts of the day when prices are high and buy energy when prices are low.

This product allows retailers and large users to manage their price risk that are increasing as the market changes with the increased penetration of intermittent generation. The deal provides 20MW of storage to Macquarie and Shell through virtual access to the stored energy.

As a risk or insurance strategy this product allows counterparties the ability to use a financial contract to replicate a battery and for battery owners the ability to hedge against their grid connected energy storage facilities.

Large-scale energy storage is currently the only option for intermittent generation such as solar and wind generators to store their excess energy when spot prices are not favorable.

This has led to an increased interest in battery storage across the National Electricity Market (NEM), with the Australian Energy Market Operator (AEMO) estimating 7,000MW of storage in the planning. The advantage of physical energy storage is that the energy can be stored when prices are low while exporting to the grid at the point when prices are high. The added benefit of physical storage is the ability for batteries to provide services to stabilise the grid when required.

As part of the planned 7,000MW of storage projects it includes the much published Snowy 2.0 which is moving ahead and the Genex storage project in North Queensland, but many other projects are not reaching financial close due to the increasing cost of pump storage hydro.

This is leading to retailers, large consumers and developers looking at other options including battery storage that is quick to build and financial products as outlined above.

Origin Energy wants to build Australia’s largest battery, announcing a 700MW battery to be built in the NSW Hunter region.

Origin Energy plans to build the battery at its Eraring Power station site south of Newcastle. The 700MW will be able to be supplied for up to four hours making it 4 times larger than the Tesla big battery, in South Australia. The battery will be built in three stages with Stage 1 to be completed by the end of 2022.

Origin recognises their role in supporting Australia’s rapid transition to renewables and a large scale batteries ability to better support renewable energy and maintain reliable supply for customers, by having long duration storage ready to dispatch into the grid at times when renewable sources are not available.

Neoen also announced last week that it plans to build a 500MW battery capable of supplying power for two hours at the site of Wallerwang Power station near Lithgo. Neoen will again use Tesla batteries, like the South Australian Big battery, and the 300MW battery near Geelong in Victoria will be capable of supplying power for half an hour.

The planned Origin and Neoen batteries would make them the two largest storage devices in the world.

With the demise of the Coal fired generation fleet it makes sense to utilise the infrastructure available at sites such as Eraring and Wallerwang to connect the batteries to the grid, but does Australia need batteries this big?

In a recent interview with the ABC, Australian Energy Market Operator (AEMO) outlined that there are now almost 7,000MW of battery storage projects in the planning process throughout Australia with the majority across the NEM.

Even with the rapid growth of renewable energy and the potential for 7,000MW of battery storage across the NEM, Snowy Hydro is still developing its gas fired power station in the Hunter Valley.

The back-up segment of the market is also showing interest from other projects including pumped hydro and compressed air energy storage which have both secured grants from the NSW Government.

With the big battery announcements and Snowy Hydros’ 750MW gas power generation, it will be interesting to see how NSW prices and volatility will fare when the two technologies fight for supremacy in the back-up energy segment of the market. NSW will continue to push for greater renewable penetration.

Understanding the spot market and spot prices is fundamental to understanding how much you ultimately pay for electricity.

The National Electricity Market (NEM) operates as a ‘spot market’. This means that supply and demand are matched instantaneously, and generators are paid a spot price for the energy they generate in any given period.

The Australian Energy Market Operator (AEMO) manages the spot market, balancing supply and demand in real time. With the safe delivery of energy the priority, AEMO controls a number of physical aspects of the market which ultimately impacts which generators are dispatched, and what spot price is achieved.

AEMO provides the market information regarding how much demand is expected. Generators compete to supply this energy by providing a bid stack to AEMO that ultimately tells the market operator how much energy they are prepared to generate for a given price. AEMO aggregates all the bid stacks from cheapest to most expensive, manages the physical requirements of the system (which stands to impact some generation with constraints, ancillary services, interconnector flows, etc.), and sets the spot price in a region at the lowest price where actual demand intersects the relevant bid stack. . All supply at and below this level is required to generate and will be paid the spot price.

Supply and demand is physically managed by AEMO varying the market in 5-minute dispatch intervals. For the purpose of financially settling the spot market, it is done in 30-minute trading intervals (an average of the six 5-minute dispatch intervals). This means the spot market currently operates in a way that physical dispatch and financial settlement are determined over different timeframes. The market was designed in this manner to incentivise slow ramping thermal generators and large users to benefit from changes to load up to 25 minutes after the price signal has been sent.

The spot market and the setting of spot prices is highly complex and governed by stringent rules for both bidding and dispatch processes (all of which go well beyond the high-level principles outlined in this article). Despite this, the dispatch and settlement timing mismatch has led to disorderly bidding practices whereby generators have been accused of ‘gaming’ the market. The Australian Energy Market Commission (AEMC) determined that in the long-term, the pricing anomaly may lead to inappropriate investment and higher prices for consumers.

Consequently, in a move to further enhance the market, from 01 July 2021 the market will start to move to 5-minute spot pricing. This means dispatch and financial settlement will be aligned, disorderly bidding will be managed, and fast response technologies such as batteries will be rewarded.

On 27 March 2020 Edge published an article written by our Senior Manager Markets & Trading, “COVID-19 / NEM Impact Statement”.

Today we revisit this article and reflect on what has transpired to date when compared to the anticipated impacts early in the pandemic.

Demand – Global and Australia

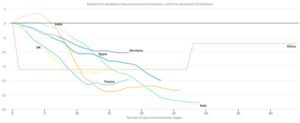

International data is starting to come through now that 2020 is behind us. From data published by the International Energy Agency (IEA) the first quarter of 2020 saw a drop of up to 20% in demand in China when full lockdowns occurred resulting in an annual reduction of 1.5%.

Globally, demand dropped 2.5% in Q120, this number may appear low but as industry dropped the demand from the residential sector increased as people were in lock down. Residential demand increased by 40% in Europe. The chart below shows the impact on demand for various regions.

It appears the reduction in demand is impacting the world in similar ways, low demands are requiring thermal plants to operate at minimum levels Rapid changes in supply when solar generation diminishes is causes ramping issues and system operators have needed to implement system security scheme to manage inertia and grid stability.

The demand profile has also changed as a result of the lockdown, a normal weekday profile now looks like a Sunday profile similar to the duck curve profile already seen in Australia.

At Home in Australia

Generation

The robustness of the Australian energy market proved itself in the early part of COVID-19 with companies such as large generators and the market operator isolating their control staff from other key staff to limit the probability of infection from other staff. These protection measures resulted in the normal operation of Power station and the grid.

Non-essential maintenance and overhauls were impacted due to COVID, as travel restrictions increased over the normal overhaul period of Q2 and Q3 this resulted in overhauls being delayed and completed in Q4 and into summer where the chance of high prices due to lower availability are much higher. The reduced availability in Q420 and Q121 has had some upside impact on the spot price with increased volatility.

Energy Prices

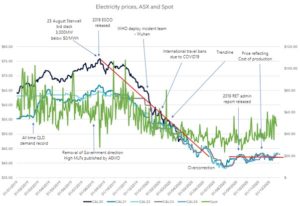

The charts below highlight the impact on energy prices in 2020. It should be noted however that prior to COVID-19 electricity prices were already decreasing. This commenced after the release of AEMO’s Electricity Statement of Opportunities (ESOO) in August 2019. The drop in spot prices and the forward market appear to be led by the increased penetration of renewables. As 2020 opened the drop was accelerated with COVID-19 dropping demand and the international trade of gas reducing, thus resulting in domestic gas prices dropping to unseen levels and generators all competing to dispatch their units.

By the 3rd quarter of 2020 the forward market levelled off at mid to high $40/MWh levels.

By the start of 2021 the international gas price also rebounded as a result of a cold winter in the northern hemisphere and potential easing of lockdowns once a vaccine is available.

With the reduced revenue available from lower contract prices, higher gas prices and increased demand following the easing of COVID-19 lockdowns, prices in the spot market started to increase and the forward market has followed.

AEMO

Through the pandemic AEMO did not have any significant issue directly associated with COVID-19, but changes did occur in AEMO’s interactions with participants. These changes resulted in AEMO sharing more information via online meetings, information sessions and consultations. AEMO’s role of the approver of connections and registration was not impacted by COVID-19 but the processes generally took longer due to the increased number of applications going through their systems.

On an operational front the lower demand and increased variability of supply and demand did challenge AEMO resulting in an increased need for AEMO to direct the market and either bring on more synchronous generation or curtail intermittent renewable generation as a result of the low demand and the increased penetration of renewables.

Demand and Change in demand – daily profile

Demand across Australia mirrored the trend seen overseas with demand in the commercial and industrial sectors dropping and the demand in residential consumption increasing. The daily usage profile also shifted with the morning peak occurring later and the evening peak becoming larger.

Impact of large users

The largest users in our market tend to be resources companies, including mining refining and the like. Consumption across the mining sector has been reduced as a result of the reductions in overseas demand for products primarily associated with power production and steel making. The downturn in production resulted in mining companies reducing or suspending operation to manage variable costs. With the growing demand for steel and increased coal fired generation in 2021 following the relaxing of lockdowns, the price of coal and Iron ore has increased leading to an increase in production approaching 2019 levels.

Renewables

As a result of travel bans and border lockdowns it become more difficult for developers to progress projects at the same pace.The construction and commissioning of renewable projects was delayed in 2020, however the market has still continued to grow. The percentage of renewable generation has increased across Australia, spot prices have dropped, and coal fired generators are being pushed out of the market due to their higher marginal cost. Emissions have also dropped over 2020 due to the reduction in thermal generation and the increased renewable generation.

LGCs

Large scale generation of renewable energy was not impacted by COVID-19 so the production of LGCs did not drop as was predicted in the early part of 2020. During 2020 Australia equalled its 2019 LGC target and when final numbers are released by the Clean Energy Regulator (CER), the target could be eclipsed.

STCs

In a similar story to the Large-scale renewable sector, the small end of the market was also not impacted by COVID-19, with roof top installations and the associated STC continuing to growth. Like LGC this year STC could exceed expectations.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.

We’re embarking on a series of posts that go back to basics. As electricity market experts, too often we come across people and / or businesses who lack an understanding of what can and can’t be done in the market. Inevitably we find that it is difficult to educate if the basics aren’t fully understood.

There is no doubt that energy markets are highly complex. For example, understanding every aspect of the National Electricity Market (NEM) is near impossible. But a solid understanding of the fundamentals is essential if you stand any chance of knowing some of the more complex aspects of it.

National Metering Identifiers

A National Metering Identifier (NMI) is a unique 10 or 11 digit number used to identify every electricity network connection point in Australia. This includes all types of metered and unmetered electricity connections to the physical electricity networks in the National Electricity Market (NEM), Western Australia markets (SWIS and NWIS) and the Northern Territory.

Learning about NMIs and their function is essential. NMIs allow all the relevant players in the market to identify your network connection point and the associated services, costs and service providers associated with it. NMIs and all the data and information associated with them, are recorded in the Australian Energy Market Operator’s (AEMO’s) Market Settlement and Transfer Solutions system (MSATS), which all key service providers have access to. Put simply, MSATS is the IT system operated by AEMO to fulfil its obligations under the National Electricity Rules (NER). We’ll post on this soon.

Via MSATS, retailers become financially responsible for your NMI in the market, and therefore the costs associated with it. The energy and market costs to AEMO, the network use of system (NUOS) costs to your Network Service Provider (NSP), and the metering costs to your metering co-ordinator (MC). Your retailer is responsible for paying these costs to the relevant providers, and then recovers these costs through charges to you in your retail energy invoice.

Meter data is collected and recorded against a NMI. Any connection related works at your premises must be done with reference to a NMI (for example the installation of embedded generation). NMIs are transferred from service provider to service provider as the preferred party for these services changes, such as retailers and metering providers.

You can find your NMI on your electricity invoice. Noting a NMI will only change if there is a change to the physical connection infrastructure (for example, a change to the connection configuration or voltage) or the physical connection is removed and then later re-established.

In terms of industry speak, NMIs are often pronounced “Nim-ees” or “N M I’s”.

In the coming posts we will focus on the installation of generation at a NMI, including small scale solar PV and larger utility scale installations. How the configuration of generation can influence your consumption requirements from the market / grid and associated regulatory impacts.

Any questions, please don’t hesitate to contact us on 1800 334 336 or email save@edgeutilities.com.au or admin@edge2020.com.au

Intertwined with Christmas and New Year celebrations, Edge2020 capped off the ‘year that was’ with excellent news regarding a 58MW renewable power purchase agreement (PPA) we brokered, and the re-signing of our longest serving and largest client.

With more renewable PPAs in the pipeline, we hope to share more good news in the coming weeks. This year we are more committed than ever to deliver consumers and generators ‘win-win’ energy solutions.

This is not all the great news we want to share. To read more about what we have been doing in the back end of 2020 and what we have in store for 2021, click the button below.

An analysis has just been released that shows the drop in Australia’s emissions due to COVID-19. This is only going to be short lived with economy returning to pre COVID-19 levels in 2021.

Although the official government emission data has not been released that cover July to September 2020, an independent report has modelled the most likely outcomes.

The report shows emissions for the first quarter of the financial year are likely to be 124.2 Mt CO2-e. It is an increase of 1.5 Mt CO2-e compared to the previous quarter, however this would still result in a reduction of 9.1 Mt CO2-e compared to the previous year.

Previously the government have indicated the current reduction in emissions will keep Australia on track to meet its Paris target, but this latest data shows the Paris target will be missed.

Emission projections for Quarter 1 of FY21 for the electricity sector were the lowest on record as far back as 2001. Demand was impacted slightly by COVID-19 but the drop in emission is linked to the growth of renewable energy and the decline of coal fired generation.

As a result of COVID-19, domestic gas prices have dropped resulting in an increase in Gas powered generation, this has resulted in more emissions from this sector.

Interestingly the reduction in emissions of around 6.8 Mt CO2-e from the electricity and agriculture sectors has been offset from emissions from stationary energy, transport, fugitive, industrial and waste sources.

The electricity sector is doing its bit to help reduce climate change, now it is up to the other CO2 producing sectors to do their bit.

Tesla has failed to reach its 2020 goal of delivering 500,000 units for the full year, but not by much. In 2019 Tesla delivered 367,500 vehicles but this year sales have increase 36%. This resulted in the company now mass producing its market favorites to meet the growing worldwide demand for EVs.

The company delivered 180,570 vehicles in the last three months of 2020. This is an increase on the previous record of 139,300 in the third quarter of 2020, to reach 499,800 sales for the year.

2020 proved to be a good year for Tesla with the company joining the SP500 and 5 quarters of growth, resulting in share increase of 743% over the year.

If the worldwide sales trajectory of EVs occurs in Australia, we will need all those charging stations to be funded by taxpayers.

Prior to the outbreak of COVID-19, Tesla was predicting sales to comfortably exceed half a million cars. By October 2020, Tesla were still confident in meeting the target even as the production facility in Northern Spring was shutdown to slow the spread of COVID-19. Apart from the Californian facilities that were temporarily shutdown, its production outside the US and primarily in China remained high. The Shanghai plant has now started producing the Model Y.

As Tesla production increases to match their rocketing share prices, other mainstream vehicle manufacturers are taking note. Large manufacturers like General Motors, Ford and VW are likely to flood the EV market with new models in the next year or two.

In an attempt to stave off competition, Tesla is setting up production lines in Berlin to compete with the European car builders and will build it’s well publicised “Pick up” in Texas.

So as we all return to work from our Christmas road trips, will more of us be driving an EV on our next road trip?

If the worldwide statistics are repeated in Australia, the answer is yes!

All we need is for the charging station networks to be built.

Often in the build up to Christmas and the New Year, politically sensitive topics are quietly released or consulted on. This year it looks like a consultation on the Climate Change Bill featured in late December.

Following the Prime Minister and the Federal Energy Ministers’ announcements that Australia was on track to ‘‘meet and beat’’ its target of 26 to 28 percent carbon reduction based on 2005 levels by 2030, various companies and lobby groups have used the consultation on the Climate Change Bill to voice their opinions.

Behyad Jafari, the Chief Executive Officer of the Electric Vehicle Council of Australia (EVC), a national body representing companies involved in providing, powering and supporting electric vehicles, has raised concerns by making a submission to the Climate Change Bill 2020.

Behyad Jafari said flawed projections on transport emissions could put the emission reduction targets in doubt.

The Morrison Government has not provided incentives to buy electric vehicles and this will jeopardise Australia’s attempts to curb transport emissions to meet international climate targets, according to EVC.

The emissions projection report released in December showed the uptake of electric vehicles is projected to increase from 1% in 2020 to 26% in 2030, however the EVC highlight that the predicted uptake of EVs by the end 2030 is too ambitious under the current energy policy.

The uptake of EVs to 26% would take 6Mt of emissions out of the transport sector.

‘‘The really disappointing thing is we have the government picking and choosing a projection to help them reach a number… It’s sort of reverse-engineering their way to say they are going to meet their climate targets’’ Mr Jafari said.

As previously reported, the electricity sector is on track to reduce its emissions by 60Mt by 2030, but other sectors such as transport and fugitive emissions from extracting mining, are not reducing their emissions but in some cases are increasing emissions through the Safeguard mechanism.

EVC argue the government’s current approach to EVs, i.e. leaving the market to determine whether people drive internal combustion engine cars or EVs would not help boost the uptake of EV’s to achieve the 26% target by the end of 2030.

Currently EVs make up 0.6% of new car purchases in Australia, compared to 3.5% worldwide. This uptake has been fueled by government policy and financial incentives to buy an EV. The UK have imposed tough policies to ban petrol cars by 2030.

As with most sectors, COVID-19 has impacted transport emissions. In 2020 transport emissions dropped by 7Mt because of lower economic activity, lockdowns and people being cautious about travel. Through 2021 and into 2022, transport activity is expected to rebound as restrictions ease. It is expected emissions will peak at 101Mt in 2026, before declining to 100Mt by 2030. The heavy transport sector, including trucks and rail were not significantly affected by COVID-19, this sector is expected to grow over the next decade and be 1Mt higher by 2030.

The EVC also argue the federal government emissions modelling did not take into account the new state taxes which studies indicate could decrease EV uptake by between 25 and 38 percent.

South Australia and Victoria are considering new taxes to help make up for the future shortfall in petrol excise through a charge per kilometre for electric vehicles to be paid by drivers annually.

Another report released at the end of 2020 was the governments Future Fuels Strategy which outlined how the Commonwealth was going to deliver charging stations for EVs. The $71.9 million fund would work with private companies to address public ‘charging black spots’. The government has previously committed $21 million towards EV charging stations along Australia’s national highways through Australian Renewable Energy Agency (ARENA).

The Future Fuels Strategy states ‘‘ensuring consumer confidence in buying new vehicle technologies is a priority for the government.’’ The government has shown interest in commercial fleets, as well as the Commonwealth’s own Comcar network, to move to EVs.

Based on where the funding is going we will have a strong network of charging stations across Australia’s national highways and a small percentage of drivers using the charging stations.

Intertwined with Christmas and New Year celebrations, Edge2020 capped off the ‘year that was’ with excellent news regarding a 58MW renewable power purchase agreement (PPA) we brokered, and the re-signing of our longest serving and largest client.

With more renewable PPAs in the pipeline, we hope to share more good news in the coming weeks. This year we are more committed than ever to deliver consumers and generators ‘win-win’ energy solutions.

For years Edge2020 has been working with leading renewable developers, financial institutions and wholesale trading counterparties to deliver consumers renewable backed products that rival standard market contracts. Whilst complex to structure and broker, they offer consumers low-cost, low risk, highly flexible and simplistic energy contracts that cannot be rivalled. We are currently aggregating loads for deals in New South Wales and Queensland, with limited opportunities available to join these transactions in early 2021.

Edge Utilities isn’t resting either, as we dive into 2021 providing both financial and physical renewable energy solutions. We’re bringing Edge2020 renewable backed deals to smaller businesses, Strata and Body Corporates. We’re also beyond excited to have partnered with a number of exceptional like-minded companies during 2020 that will allow us to deliver behind-the-meter solar solutions to low and medium rise commercial and residential strata complexes. We’ll be combining these financial and physical products to deliver unprecedented renewable energy solutions to this segment of the market. And to say we are excited about it, is an understatement!

We want to make our goals for 2021 crystal clear. We want all consumers to be more informed. We want you to genuinely understand the energy deals that you are presented with – the good, the bad, and the downright ugly. We want you to pursue opportunities that deliver genuine cost savings, not just perceived savings. And in doing so, we want you to help save our planet.

Let us do the hard work for you. Let us bring you the benefits of decades of energy market expertise and strategic relationships, and trading and brokering billions of dollars of energy deals for some of the largest names you can think of.

Hydro Tasmania have signed its first deal for the energy stored in its system.

Hydro Tasmania have signed its first deal for the energy stored in its system. Hydro Tasmania have signed its first deal for the energy stored in its system.

Hydro Tasmania have signed its first deal for the energy stored in its system. Origin Energy wants to build Australia’s largest battery, announcing a 700MW battery to be built in the NSW Hunter region.

Origin Energy wants to build Australia’s largest battery, announcing a 700MW battery to be built in the NSW Hunter region.

et (NEM) is near impossible. But a solid understanding of the fundamentals is essential if you stand any chance of knowing some of the more complex aspects of it.

et (NEM) is near impossible. But a solid understanding of the fundamentals is essential if you stand any chance of knowing some of the more complex aspects of it.

An analysis has just been released that shows the drop in Australia’s emissions due to COVID-19. This is only going to be short lived with economy returning to pre COVID-19 levels in 2021.

An analysis has just been released that shows the drop in Australia’s emissions due to COVID-19. This is only going to be short lived with economy returning to pre COVID-19 levels in 2021. Tesla has failed to reach its 2020 goal of delivering 500,000 units for the full year, but not by much. In 2019 Tesla delivered 367,500 vehicles but this year sales have increase 36%. This resulted in the company now mass producing its market favorites to meet the growing worldwide demand for EVs.

Tesla has failed to reach its 2020 goal of delivering 500,000 units for the full year, but not by much. In 2019 Tesla delivered 367,500 vehicles but this year sales have increase 36%. This resulted in the company now mass producing its market favorites to meet the growing worldwide demand for EVs. Intertwined with Christmas and New Year celebrations, Edge2020 capped off the ‘year that was’ with excellent news regarding a 58MW renewable power purchase agreement (PPA) we brokered, and the re-signing of our longest serving and largest client.

Intertwined with Christmas and New Year celebrations, Edge2020 capped off the ‘year that was’ with excellent news regarding a 58MW renewable power purchase agreement (PPA) we brokered, and the re-signing of our longest serving and largest client.