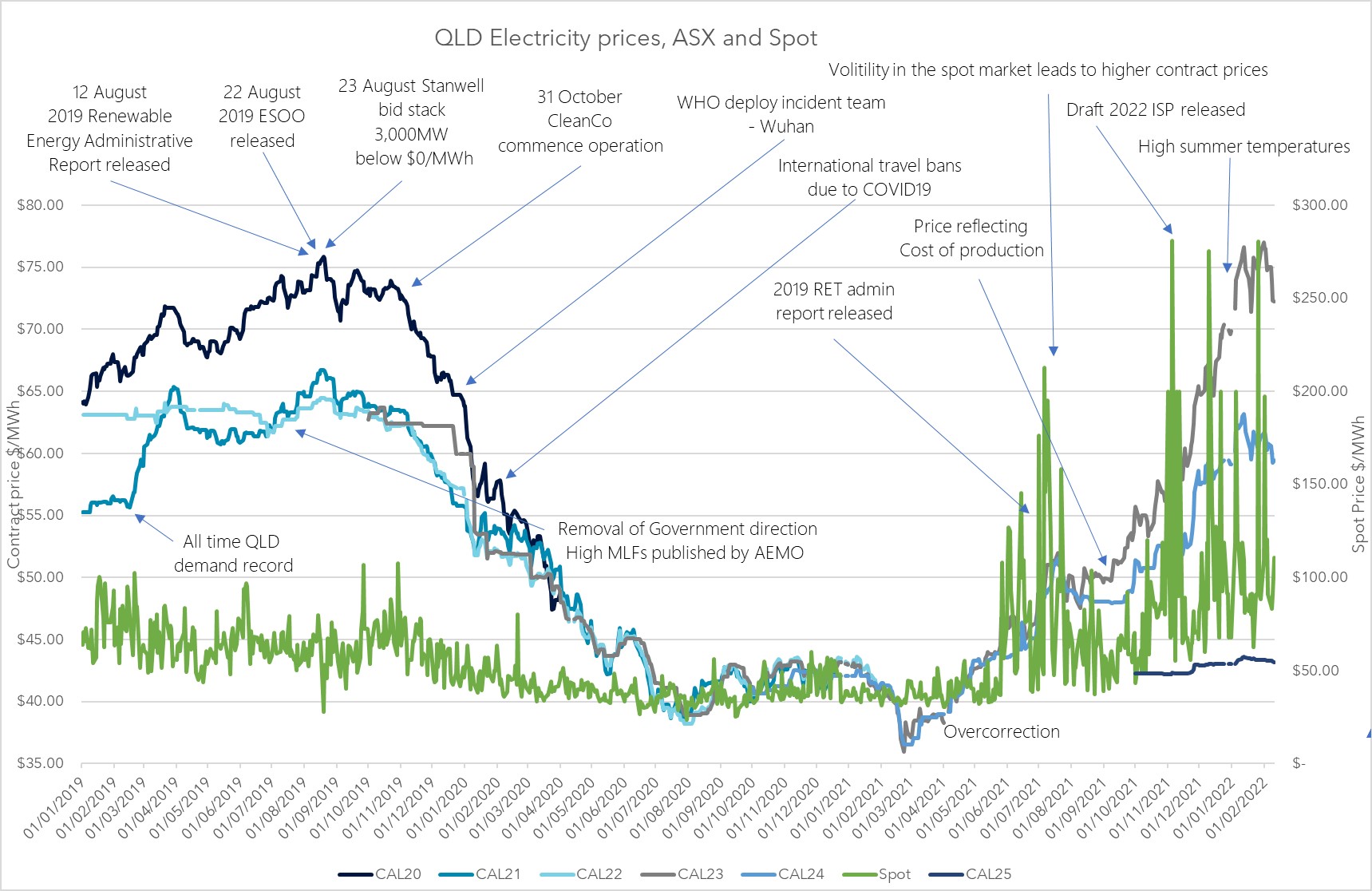

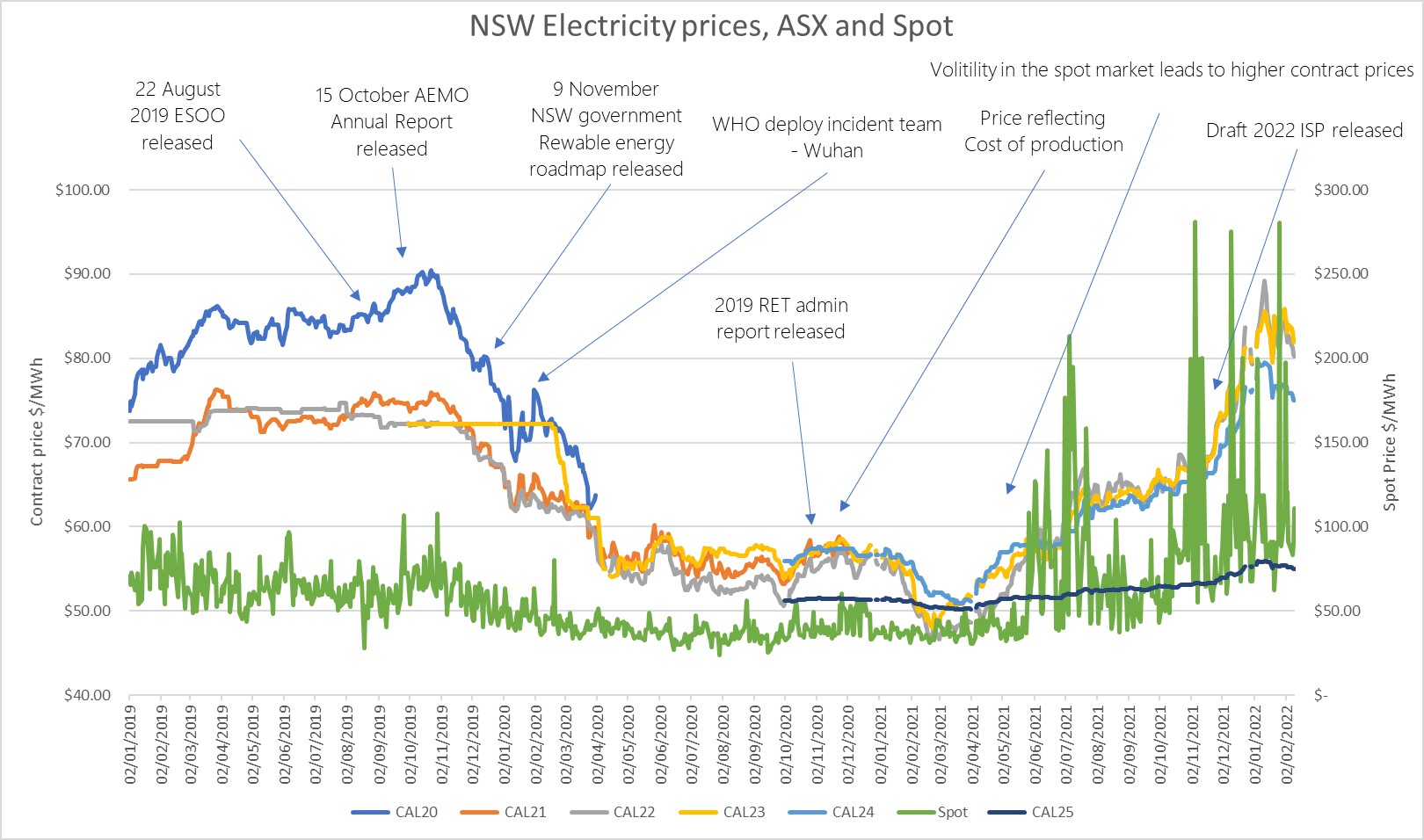

Last week the Clean Energy Regulator (CER) released its targets for liable entities to meet their Large scale Generation Certificate (LGC) and the Small scale Technology Certificate (STC) obligations for 2022.

The 2022 Renewable Power Percentage (RPP) was set at 18.64%, up marginally from 18.54% in 2021.

The 2022 Small scale Technology Percentage (STP) was set at 27.26%, down marginally from 28.80% in 2021.

What are these targets?

These targets are set under the Renewable (Electricity) Energy Act to stimulate and support the development of renewable electricity production in Australia.

Liable entities are individuals or companies who make relevant acquisitions (mostly the purchase of wholesale electricity) from a grid with an installed capacity greater than 100MW. Liable entities are most commonly electricity retailers. Under the Renewable Energy Target (RET) legislation, liable entities are required to surrender a specified volume of certificates equivalent to a set percentage of their relevant acquisitions across the year.

There are two types of certificates under the RET, LGCs and STCs. The percentage of LGCs required to offset relevant acquisitions is set by the RPP, and for STCs it is set by the STP. Retailers produce or procure certificates and surrender them to the CER to meet their liabilities. They then pass on the costs associated with meeting these liabilities to retail customers based on their proportional contribution to the relevant acquisitions.

What do these targets mean for large users?

The key point to understand is that in most situations the liable entities are the retailers. But a retailer’s liability is directly derived from what is consumed by the retail customers. Each user’s contribution to a retailer’s liability can be calculated utilising the relevant liability percentages, and the consumer’s loss adjusted gross consumption.

The higher the RPP and STP the greater the percentage of a customer’s usage needs to be covered by the relevant certificates. Assuming a customer’s annual consumption remains on par from one year to the next, higher liability percentages result in more certificates being required to offset that user’s contribution to a retailer’s liability.

Can large users control the costs associated with these targets?

Short of reducing consumption, users cannot control the number of certificates that their retailer will need to cover their contribution to the retailer’s liability. These percentages are regulated.

Emissions Intensive and Trade Exposed (EITE) users can apply for exemptions through the CER. These are issued in the form of Partial Exemption Certificates (PECs) that when provided to the liable entity can be used to directly offset the liability.

Large commercial and industrial users can negotiate electricity sale agreements with their retailers that allow them to proactively work with retailers to determine how and when certificates are obtained by the retailer to meet the liabilities associated with that user. This can involve the user having the ability to instruct the retailer when to purchase or price a set quantity of certificates, or to self-surrender certificates acquired or produced elsewhere by the user to the retailer, or to ask the retailer to sleeve third-party agreements (such as renewable power purchase agreements – PPAs) negotiated by the user to facilitate the provision of certificates at prices and terms negotiated by the user.

Where do these certificates come from?

LGCs are created by accredited power stations that produce electricity from renewable energy sources. For every megawatt hour (MWh) of electricity produced from renewable sources equals one LGC.

STCs are created by eligible energy systems. Like the LGC an STC is equivalent to 1 MWh of renewable electricity produced, however, the number of STCs a system can produce is calculated over a period of 1 to 10 years based on the technology. STCs can be produced by rooftop PV systems, small scale wind and hydro and even the electricity displaced by a solar water heater or heat pump over its lifetime.

How are these certificates traded?

LGCs can be acquired by purchasing them directly from renewable energy power producers or through the secondary market. The price of LGCs can vary depending on if the certificates are acquired via the market or directly from the project, and if they are settled and transferred upon entering a transaction (spot) or at some time in the future (forward contracts). Currently, the spot LGC price is around $46 per certificate, and the forward curve for LGCs falls away year on year.

Once an STC is created it can be traded through the STC market or through the STC clearinghouse. The STC clearinghouse is operated by the CER with a set price of $40 per certificate. It’s operated on a first in first served basis, which means sellers need to join the end of the queue and wait for their turn to sell. The market is more liquid and affords sellers the ability to sell certificates once a deal is negotiated. The price of a certificate is based on the supply/demand balance, with STCs currently trading around $39.40 per certificate.

What can I do to reduce my costs associated with LGCs and STCs?

Like many large users that aren’t already managing these components, your costs are no doubt going up. This doesn’t have to be the case. If you’re a large energy user, reach out to our team. We can assess your portfolio and certificate requirements, how you currently get charged for these components, and advise how you can be better manage this with your retailer.

Edge2020 traded over 1.75 million LGCs and 1.17 million STCs in 2021 for our portfolio of large users. These were either managed through retail sale agreements or directly with renewable producers through power purchase agreements (or similar).

Our team are specialists in ensuring large users minimise their costs utilising products and strategies that deliver value. These products may be a pass-through cost for retailers, but that doesn’t mean they shouldn’t be managed and minimized. We work closely with retailers, in a collaborative and positive manner to achieve outcomes that reduce their costs whilst not impacting their operational processes or retail returns.

Send us a message or contact us through Lolita at lolita.rainsbury@edge2020.com.au.

We look forward to talking with you.